Hardware Hits Mega-Round Season Again: Whoop’s $575M at $10.1B, Neuralink at $9.7B, BrainCo’s $1.3B Unicorn Birth, eMed’s $200M Series A at $2B, and Whether Consumer Hardware Is Back

Welcome to Healthcare Markets & Technology.

Rigorous analysis of AI, policy, capital, technology, and clinical operations across U.S. healthcare — written for the people who build, invest in, and lead it.

Free subscribers get 2 public articles per week. Upgrade to paid → for the full 7 articles/week, paid podcast episodes, deal breakdowns, and the complete 538-deep-dive archive.

Subscribe or upgrade here →

One thing to bookmark: the searchable Knowledge Base at kb.onhealthcare.tech isn’t in Substack’s menu. Save it now — on mobile, tap share → “Add to Home Screen.”

Reply to any email with questions. I read every one.

— Trey

Video Preview

Podcast, Part I (Free)

Podcast, Part II (Paid)

To listen to paid episodes in Apple or Spotify, link your Substack subscription via the show settings on those platforms (instructions inside the Substack app under Subscriptions → Podcast).

Abstract

Q1 2026 minted four hardware-driven digital health mega-rounds in a single quarter. Whoop closed $575M at $10.1B, Neuralink got marked at $9.7B, BrainCo raised $272M at $1.3B in a unicorn-birth round, and eMed pulled a $200M Series A at $2B. Add Oura sitting at $11B and Verily’s $300M from Alphabet’s syndicate, and four of the top ten digital health unicorns by valuation now run on atoms rather than bits. The bull pitch is different this cycle: subscription stacks on top of hardware, FDA-cleared diagnostics moving over-the-counter, sovereign BCI plays out of China, and platform partnerships with academic medical centers. The bear pitch is that capital is concentrating violently (mega-rounds took ~61% of all digital health funding across just 19 deals) and this is what cycle tops have always looked like. Either consumer hardware is back or this is the marker top.

Table of Contents

How the last hardware cycle ended

The Q1 receipts

Whoop, Oura, and the wrist-versus-ring fight

The brain interface bracket

eMed, Verily, and the at-home diagnostic comeback

What the hiring data is whispering

Either hardware is back or this is the top

How the last hardware cycle ended

The hardware bear thesis was earned, not invented. Peloton peaked around $171 a share in early 2021 and was trading under $4 by mid-2024, with three CEOs cycled through and a strategic review that produced no buyer at any price anybody could justify to a board. Lululemon paid roughly $500 million for Mirror in 2020, wrote the whole thing down a couple of years later, and quietly shuttered the standalone Mirror operation entirely. Fitbit got absorbed into Google, where its hardware roadmap promptly went on the kind of long hiatus that always precedes a Google product cull. Pear Therapeutics, which sat adjacent to hardware as a prescription digital therapeutics distributor, ran out of cash in 2023. 23andMe went into bankruptcy and is currently in the awkward process of having its one and only valuable asset, a few million spit-tube genomes, parceled out by a court. Theranos and the IPO-era diagnostics startups had poisoned the well for at-home dx years before that, and the consumer hardware category as a whole spent most of 2022 through 2024 in what one tier-one healthcare investor privately described as the penalty box.

The lesson VCs took from that wreckage was the usual one. Hardware is hard. Margins compress, return horizons stretch, channel costs eat you alive, FDA pathways turn into years of cash burn, and the moment you hit any scale the platform companies decide whether you live or die. Apple was the chief executioner here. Each new Apple Watch generation rolled up another adjacent health category. Blood oxygen, EKG, sleep tracking, atrial fibrillation detection, fall detection, sleep apnea screening, and most recently FDA-cleared hypertension monitoring all came stock on the wrist. Every release left some hardware startup wondering whether they had just been Sherlocked.

By late 2024 the consensus take was that any consumer-facing health device without either a regulatory moat (FDA-cleared diagnostic claim, ideally with a CPT code attached) or a closed clinical loop (real provider workflow, real reimbursement) was going to get bundled into oblivion. So when the first quarter of 2026 produced a string of nine and ten-figure hardware rounds, the question wasn’t whether the data was real. The question was whether late-stage capital had seen something the prior twenty-four months of consensus had missed, or whether the dollars had simply run out of better places to go.

The Q1 receipts

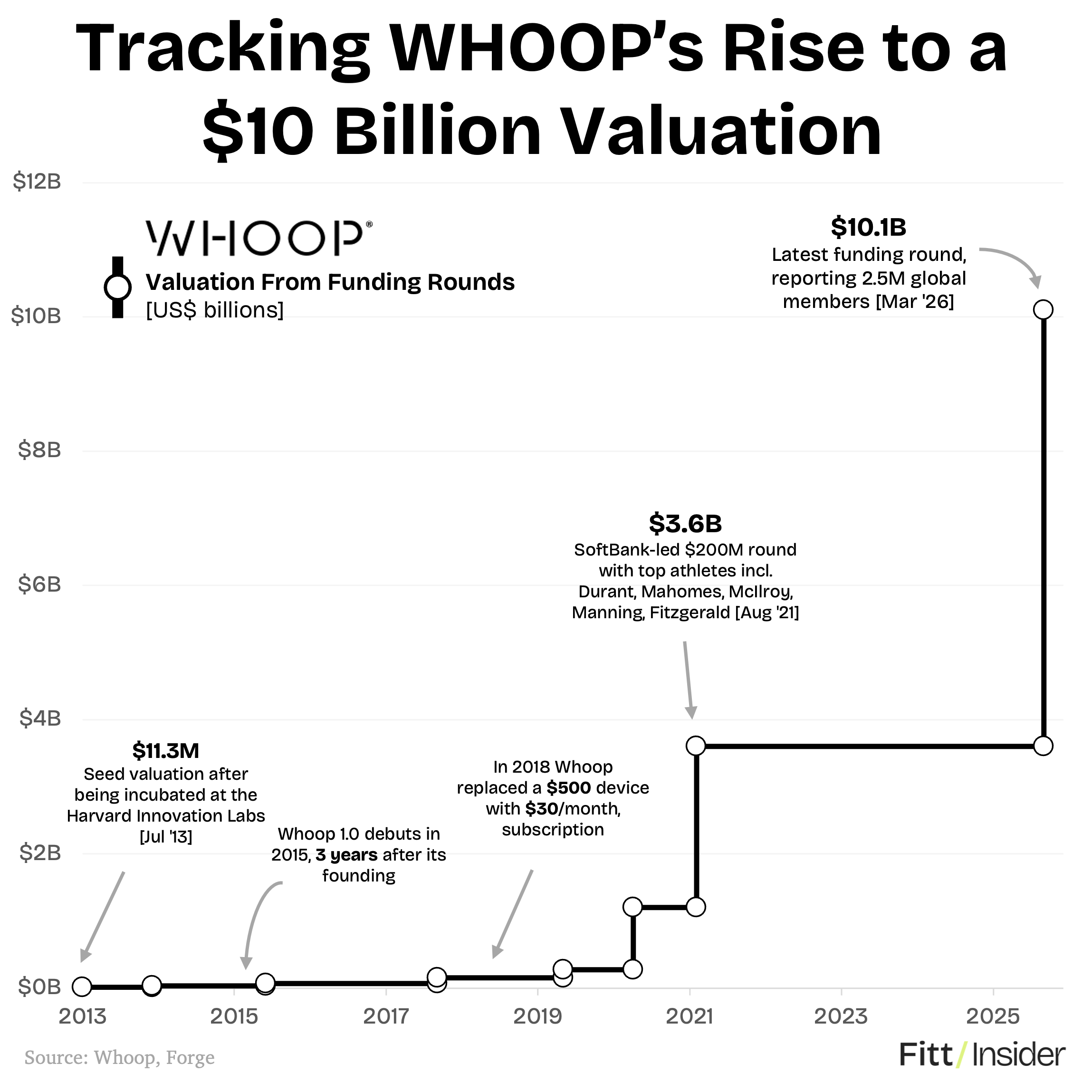

Start with the Whoop number because it’s the loudest. The Boston company closed $575M in a Series G at $10.1B, with Collaborative Fund and Institutional Venture Partners leading, Accomplice and Foundry alongside, and a sprinkle of athletes including Cristiano Ronaldo, which is the kind of cap table that either signals the end of an era or the start of one and is rarely ambiguous in retrospect. Whoop’s last public mark was around $3.6 billion in mid-2021. So this is roughly a 2.8x in five years, which doesn’t sound spectacular on its own, until anyone remembers that essentially every peer consumer health company is sitting at a meaningful discount to its 2021 marks. Whoop is up. Valuation per employee here lands around $7.7 million, on a headcount of roughly 1,300.

Oura is at roughly $11 billion as a private out of Finland and has now earned the unofficial title of unicorn-that-wouldn’t-die. Neuralink got marked at $9.7 billion. BrainCo, a Chinese brain-computer interface company that started its life selling EEG focus headbands and has been steadily migrating toward more medically serious territory, closed $272M in a Series B at a $1.3B unicorn-birth valuation, with IDG Capital, Walden International, Dowstone, and Huazhu Group writing checks. eMed, the at-home diagnostic platform that started life verifying COVID rapid tests over proctored video, raised $200M in a Series A at a $2 billion valuation with Aon, Antonio Gracias, Jeff Aronin, Ara Cohen, and Joe Lonsdale on the cap table, which reads more like a private aviation manifest than a typical healthtech investor list. Verily, the Alphabet life sciences spinout that has pivoted somewhere between three and six times depending on whose count is canonical, raised $300M from a syndicate including Series X Capital, Alphabet itself, the University of Colorado Anschutz Medical Campus, and UCHealth.

Round out the picture with Ultrahuman’s $48M Series C out of India, Stairmed’s $73M Series C in China (another BCI play, this one backed by Alibaba, Lilly Asia, OrbiMed, and FountainBridge Capital), Monteris Medical’s $28M Series E for laser-based brain surgery, XCath’s $30M Series C, Omniscient Neurotechnology’s $13M Series D out of Australia, and a handful of smaller pickups in surgical AR/VR and neuromodulation. Hardware founders did not skip lunch this quarter.

Whoop, Oura, and the wrist-versus-ring fight

The thing about Whoop and Oura is that neither one really sells hardware in any economic sense a traditional consumer electronics company would recognize. Whoop’s pitch since the original strap launched has been that the device is the cost of entry to a subscription. The hardware itself is included with the membership at no marginal sticker price, the company makes its money on recurring revenue, and the underlying unit economics look closer to a SaaS business with a logistics overhead than to a Fitbit. Oura takes the opposite packaging approach (the ring sells outright at full retail, the boxes show up in Best Buy displays and on the Amazon home page) but has been steadily layering subscription on top, with the current product effectively requiring an Oura Membership to unlock the analytics that justify the device in the first place.

The point is the same. Both companies own the post-purchase relationship with the user, both have data feedback loops that compound over time, and both have started building clinical research and enterprise partnerships that traditional CE companies would never get near. Oura’s relationships with the Cleveland Clinic, the Department of Defense, and a long list of academic research groups suggest the ring is quietly becoming a research-grade data collection platform whether the company set out to be one or not. Whoop sells into pro sports and special operations the way Bloomberg sells into hedge funds, which is to say at full price, with a deeply embedded customer base, and with switching costs that compound the longer the data history runs.

Both have kept growing in the face of Apple Watch feature creep precisely because they are not actually competing for the same purchase decision. The Apple Watch wins as a smartwatch with health features attached. Whoop and Oura win as health devices with no smartwatch features at all. That distinction looks pedantic until somebody actually wears a device that doesn’t beep at them during a meeting. The hard question is whether either company can grow into a $10 billion or $11 billion mark on subscription economics alone, or whether the implicit thesis baked into these valuations is that they will need to expand into adjacent revenue streams. Continuous glucose monitor integrations, longevity testing kits, women’s health analytics, enterprise wellness contracts, and clinical research data licensing are all on the menu. Both companies have been telegraphing platform ambitions for a couple of years. The Q1 round size and timing suggests their investors believe they are close enough to inflection on at least one of those adjacencies to justify writing big checks now rather than waiting another twelve months. If that read is right, Whoop and Oura are not really wearables companies anymore. They are health data platforms with wearables as the customer acquisition mechanism, which is a very different multiple regime than the one Fitbit got priced on the way out the door.

The brain interface bracket

Then there is the BCI cohort, which is its own animal entirely. Neuralink crossed the first-patient threshold in early 2024 with Noland Arbaugh, has done additional implants since, and got marked at $9.7 billion in this cycle. The clinical milestone matters less here than the narrative milestone. For roughly a decade, BCI was a category that had to apologize for itself in front of LPs. Every BCI deck had to spend three slides explaining why this time was different from the DARPA-funded BCI cycle of the late 2000s. Neuralink’s clinical demonstrations, combined with Elon Musk’s willingness to absorb regulatory and reputational risk that other founders simply could not, forced the category back onto the agenda whether the rest of the field liked it or not.

BrainCo’s $1.3 billion mark sits in an interesting place. The company started its commercial life selling EEG-based focus-training headbands into Chinese schools, which got it some unflattering international press a few years back when photos surfaced of classrooms of kids wearing what looked like compliance-monitoring devices. The medical roadmap has since migrated toward more serious targets including stroke rehab, prosthetic control, post-injury neural retraining, and clinical-grade neural monitoring. The capital backing in this round is almost entirely Chinese, which is part of the story. China is running a deliberate parallel BCI development effort that does not depend on FDA timelines or American patient enrollment, and BrainCo and Stairmed together are the most visible expressions of that policy. Stairmed has reportedly done its own first human implant with an invasive electrode system, with partnership backing from Tsinghua, which puts the Chinese BCI cohort meaningfully closer to Neuralink in clinical progress than most American investors have priced into their models.

The bull case for the bracket is that BCI is roughly where medical robotics sat around 2010, when Intuitive Surgical was the only name with a credible installed base and nobody quite believed there would be a serious second-mover ecosystem. There is now a second-mover ecosystem in surgical robotics worth tens of billions in aggregate enterprise value, with Stryker, Medtronic, Smith and Nephew, and a long tail of category-specific players. If BCI follows even a fraction of that arc, the names hitting unicorn status in 2026 are candidates for the Stryker-of-BCI position a decade out. The bear case is that BCI carries device-failure modes that have no real analogue in surgical robotics. Electrode degradation over multi-year horizons, biocompatibility of materials sitting in cortical tissue, the small matter of cracking open a skull every time the firmware needs a redesign, and a regulatory pathway that has barely been written. Reimbursement is somewhere between hypothetical and aspirational. The companies pricing in this quarter are pricing in a future state that may or may not show up on the timeline the cap tables are betting on.

eMed, Verily, and the at-home diagnostic comeback

eMed is a more confusing valuation to assess. The company built its initial revenue base verifying at-home COVID antigen tests over proctored video, which was an extraordinarily clean monetization line during the pandemic and largely went away with it. The Series A at $2 billion with 604 employees and an investor lineup of Aon plus a who’s who of the Joe Lonsdale and Antonio Gracias orbit suggests the company has reassembled around a broader at-home diagnostics platform play. Best read of the strategy is some combination of GLP-1 prescribing workflows, weight loss and metabolic health programs, and verified at-home testing across categories that insurers and self-insured employers will actually reimburse. Valuation per employee here lands around $3.3 million, which is on the high side for a services-adjacent business but not absurd if the recurring contract book with payers and employers is as deep as the round size implies.

Verily is the original Alphabet life sciences vehicle and at this point the running joke in any conversation about pivot economics. The contact lens that was supposed to measure glucose in tears did not work. The mosquito releases did. Onduo got folded back into a partner. Coefficient Insurance got sold off. The current incarnation centers on a clinical research platform plus precision health offerings to health systems, and the $300 million round with UCHealth and Anschutz participating points toward that focus. Whether the round is a vote of confidence in the latest strategy or a bridge structured to keep optionality open while Alphabet figures out what it actually wants to do with the asset is genuinely ambiguous, and the syndicate composition can be read either way.

The bigger at-home diagnostics story across this quarter sits underneath the eMed and Verily headlines, which is the mainstreaming of continuous glucose monitors for non-diabetic use. Dexcom’s Stelo and Abbott’s Libre Rio both launched over-the-counter products targeting metabolic health rather than glycemic control. Function Health, Hims, Hers, Levels, and a growing tail of metabolic health subscription products run software wrappers on top of lab panels and CGM data. The hardware companies underneath those wrappers, namely Dexcom, Abbott, Roche, and BD, are public, large-cap, and not in any private market data set, but their wholesale shift toward consumer channels is the most important atom-level story in consumer health right now. It is also what allows the eMed and Verily rounds to look defensible rather than ridiculous. Hardware-derived diagnostic data has finally crossed a usability threshold where consumers will pay for the readouts and providers will accept the inputs into clinical decisions. Five years ago that was not true.

What the hiring data is whispering

The other thing worth pulling out is what the headcount data has been doing in the background while the deal headlines were busy. Healthcare humanoid robot developers ran roughly a thirty-four percent year-over-year headcount increase. Neuromodulation device companies were up about twenty-five percent. Fitness tracking apps and sleep tracking devices clocked something close to twenty-four percent each, and AR/VR surgical guidance and navigation companies were up around twenty-two percent. Healthcare AI model developers led the entire digital health tape at almost fifty-nine percent year-over-year headcount growth, but the hardware-adjacent categories were sitting right behind them. That pattern is notably different from the three prior years, where headcount growth was concentrated almost entirely on the software side and hardware companies were quietly thinning out engineering rosters.

The engineering labor flow tells the bull story better than the deal data does because it’s harder to fake. Mid-career poach activity in mechanical engineering, electrical engineering, firmware, embedded ML, and biomedical signal processing has visibly picked up. Stock-comp dilution at private hardware companies has reset upward, which is the kind of move only made when a company genuinely believes it is staging for a multi-year product roadmap and needs to compete for talent with model-developer roles that pay top of market. Hardware companies that thought they were hitting a wall in 2023 reversed course in 2025, and the talent market is reflecting that reversal in roughly real time.

Either hardware is back or this is the top

Which leaves the actual question, which is whether this is the start of a multi-year hardware cycle or the kind of late-cycle exuberance that gets remembered as a marker top once funding conditions turn. The honest answer is that both reads are defensible and that the meaningful resolution will not come from another quarter of data.

The bull case rests on two structural shifts that did not exist in the prior cycle. The first is that ambient and continuous sensing technology actually works now in a way it did not in 2017 or even 2021, because the on-device ML compute and the model architectures finally caught up to what the sensors can produce. The second is that the regulatory and reimbursement landscape for hardware-derived data has loosened materially. CGM over-the-counter clearance, Apple Watch hypertension clearance, FDA’s continued willingness to greenlight software-as-a-medical-device built on top of sensor outputs, and the slow but real movement of CMS toward reimbursing remote patient monitoring built around consumer-grade devices have all moved the underlying unit economics. Hardware companies are finally able to charge for what they produce, and increasingly they can charge two or three different counterparties for the same data stream, which is what a real platform business looks like in practice.

The bear case is that valuation discipline rarely survives a quarter like this one. Mega-rounds captured something like sixty-one percent of all digital health funding in Q1, a record concentration, and that capital crowded into just nineteen deals. That kind of concentration tends to produce its own narrative ratification. The investors writing the Whoop check believe Whoop is worth ten billion because their fellow investors believe Whoop is worth ten billion, and the private secondary markets that would normally provide an external sanity check are themselves dominated by the same fund managers writing the primary checks. None of these private hardware companies have disclosed financials, and the mark-to-mark mechanics across cap tables can absorb a lot of optimism before reality intervenes. Hardware has always required more capital and longer return horizons than software, and the temptation to mark up paper at the top of a cycle is exactly the kind of behavior that produces the Peloton stories in a few years.

The most honest read might be that the names raising in this quarter are not the ones to worry about. Whoop’s subscription book, Oura’s enterprise pipeline, Dexcom’s and Abbott’s CGM channel work, and Neuralink’s clinical pipeline all point to real underlying progress that the capital is rewarding. The companies to watch for the top signal are the second derivatives, the pile-in rounds that will appear in the next two quarters across the same categories at the same prices without the same earned right to be there. That’s where the top will get marked, if it gets marked at all. For now the wearable and BCI and at-home dx categories all look meaningfully more durable than they did eighteen months ago, and the dollars are flowing accordingly. Whether they should be is a question whose answer is two years away and probably won’t be obvious until somebody’s lead investor stops returning calls.