What does 17 pharma MFN deals are underneath the press releases: the real primary source stack, the GLP1 numbers, TrumpRX plumbing, and where the new adjudication layer gets monetized

Welcome to Healthcare Markets & Technology.

Rigorous analysis of AI, policy, capital, technology, and clinical operations across U.S. healthcare — written for the people who build, invest in, and lead it.

Free subscribers get 2 public articles per week. Upgrade to paid → for the full 7 articles/week, paid podcast episodes, deal breakdowns, and the complete 538-deep-dive archive.

Subscribe or upgrade here →

One thing to bookmark: the searchable Knowledge Base at kb.onhealthcare.tech isn’t in Substack’s menu. Save it now — on mobile, tap share → “Add to Home Screen.”

Reply to any email with questions. I read every one.

— Trey

Table of contents

Where the 17 actually comes from

The executive order and the pressure step

Pfizer through AstraZeneca and the deal template

The Lilly and Novo GLP-1 deal as the actual main event

The December nine and the J and J pickup

TrumpRx and what is actually live on the page

Regeneron and the closing of the cohort

What is in the deals and what is conspicuously missing

IRA plus MFN as a quasi-voluntary hybrid

The new adjudication layer and where the infrastructure gets built

Open questions, gaps, and what to watch next

Abstract

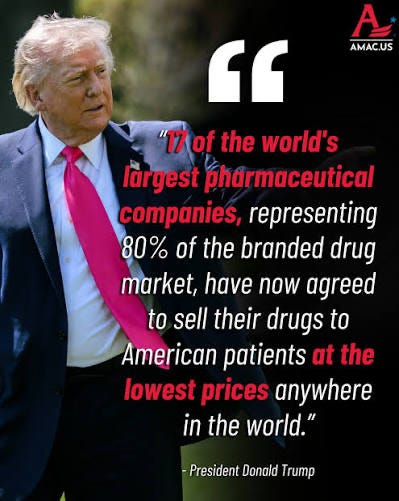

The viral “17 pharma companies” claim circulating off the recent White House posts is real, but the actual evidence base is fragmented. There is no consolidated White House list. The cohort has to be reconstructed from three layers: the July 2025 demand letters, the rolling deal announcements from Sept 2025 through April 2026, and reporting filling in the gaps. Cohort: AbbVie, Amgen, AstraZeneca, Boehringer Ingelheim, BMS, Lilly, EMD Serono, Genentech, Gilead, GSK, J&J, Merck, Novartis, Novo, Pfizer, Regeneron, Sanofi. Roughly 86% of branded drug market by the admin’s own framing. Key pricing data points: GLP-1s at ~$245 Medicare/Medicaid, ~$350 TrumpRx cash, $50 Medicare copay; Praluent cut from $537 to $225; Otarmeni free in the US. Important caveats: deals are bilateral and confidential; no published contract text, no reference country basket, no MFN formula, no state Medicaid implementation guidance, no drug-by-drug schedule. The actual investment angle is the new adjudication layer this creates: MFN benchmarking engines, compliance tooling, Medicaid plus DTC routing, employer fiduciary analytics, and drug-level channel arbitrage. None of that infrastructure exists at production scale today.

Where the 17 actually comes from

The first thing to flag is that the canonical list of 17 does not live in any single White House document. There is no master PDF, no consolidated dataset, no clean spreadsheet sitting on whitehouse dot gov with seventeen rows. Anybody trying to chase down the actual cohort has to reconstruct it from three different layers stacked on top of each other. Layer one is the original demand letter cohort from July 2025. Layer two is the rolling sequence of deal announcements that came out from September 2025 through April 2026. Layer three is third-party reporting filling in the gaps where the administration did not bother to publish anything formal.

The seventeen companies, once stitched together from those three layers, are AbbVie, Amgen, AstraZeneca, Boehringer Ingelheim, Bristol Myers Squibb, Eli Lilly, EMD Serono (which is the US arm of Merck KGaA, not the US Merck, and yes the naming convention is annoying), Genentech (the Roche subsidiary), Gilead Sciences, GSK, Johnson and Johnson, the US Merck, Novartis, Novo Nordisk, Pfizer, Regeneron, and Sanofi. That collection represents around eighty-six percent of the branded drug market by the administration’s own framing in the final Regeneron fact sheet. Everything that gets discussed under the MFN umbrella traces back to that group. Anyone trying to reason about which manufacturers are exposed, which therapy classes get hit first, or which channels are most likely to see margin compression needs to start with the seventeen-company anchor.

The reason this matters is not academic. The deal-by-deal language varies a lot, the therapeutic categories vary a lot, and the publicly disclosed pricing methodology varies even more. But the cohort itself is the constraint, and any analytical work on this program that does not sit on top of that cohort is going to be either too narrow or too broad to be useful.

The executive order and the pressure step

The legal scaffolding starts with the May 12, 2025 executive order on most-favored-nation prescription drug pricing. That order does three things that matter. It directs HHS to set MFN targets across products and channels. It enables direct-to-consumer sales structures designed to bypass the traditional PBM-intermediated path. And it threatens rulemaking if voluntary progress from manufacturers fails to materialize. That last piece is the actual lever. Voluntary programs in healthcare almost never work on their own merits, but they work fine when the alternative is a slower and more painful regulatory process the manufacturer cannot easily fight in court.

Two and a half months later, on July 31, 2025, the White House put out a fact sheet saying that manufacturer proposals had fallen short and that letters had been sent to the leading manufacturers spelling out what they needed to do. That is the moment the seventeen-company cohort becomes a real thing rather than a rhetorical target. The pressure structure is straightforward. The administration has tariff authority, executive order authority, and rulemaking authority. The threat package is broad enough that the rational play for a multinational pharma company is to come to the table and shape the deal rather than litigate it.

The other detail worth flagging from the July step is the framing around foreign revenue repatriation and US manufacturing investment. The deals are not just about Medicaid pricing. They are bundled with implicit and explicit commitments around onshoring production capacity, exempting certain pharmaceutical inputs from tariffs, and making sure the US-priced channels do not subsidize cheaper international markets indefinitely. That bundling is what makes the program politically durable, because it ties drug pricing into the broader trade and industrial policy stack rather than letting it sit as a one-off pricing reform that a future administration can easily unwind.

Pfizer through AstraZeneca and the deal template

The first actual deal landed with Pfizer on September 30, 2025. That fact sheet is the single most important primary source for anybody trying to understand what these MFN agreements actually contain, because every subsequent deal is roughly a variation on the Pfizer template. The Pfizer agreement covered four buckets. First, Medicaid gets MFN access on Pfizer’s portfolio. Second, all of Pfizer’s new innovative medicines get MFN pricing at launch. Third, Pfizer commits to a foreign revenue repatriation structure. Fourth, Pfizer offers DTC discounts through what would later become the TrumpRx platform. The fact sheet specifically named Eucrisa, Xeljanz, and Zavzpret as included products, which gives a useful read on how the administration was thinking about scope. It was not just specialty drugs and not just primary care. It was a mix of inflammatory, eczema, and migraine products, which suggests the channel logic was driven more by what Pfizer wanted to put on the table than by any clean therapeutic category.

The AstraZeneca deal followed in October 2025 as the second MFN agreement. That fact sheet did three useful things. It confirmed that the July letters had gone to the leading manufacturers, which is one of the few places the administration explicitly tied the September deal to the July pressure step. It validated that the Pfizer template was going to be the running pattern. And it provided the first signal that the deals were going to be cumulative rather than one-off, with each new agreement adding to the same MFN framework rather than spinning up a new structure.

That second deal is also where the bilateral and confidential nature of the agreements starts to become a real analytical problem. The fact sheets describe what is in each deal at a high level, but there is no published contract text, no reference country basket, no MFN calculation methodology, and no drug-by-drug pricing schedule. That gap stays open through every subsequent deal and is one of the central things AMCP flagged in its later analysis.

The Lilly and Novo GLP-1 deal as the actual main event

The November 2025 announcement covering Eli Lilly and Novo Nordisk is the commercial center of gravity for the entire program, even though structurally it is just one of the seventeen tranches. The reason is obvious to anybody who has been watching GLP-1 economics for the last three years. The GLP-1 class is the biggest pricing and volume story in pharma in a decade, with Ozempic and Wegovy from Novo and Mounjaro and Zepbound from Lilly running combined US revenue numbers that rival some entire therapeutic categories. Anything that touches that pricing structure has implications that ripple through PBM economics, employer plan design, formulary positioning, supplemental rebate dynamics, and the broader specialty pharmacy infrastructure.

The named products in the Lilly-Novo deal include Ozempic, Wegovy, Mounjaro, Zepbound, future oral GLP-1 formulations, Emgality, Trulicity, NovoLog, and Tresiba. The pricing structure is where it gets interesting. Medicare and Medicaid prices for some GLP-1s land at $245 per month. TrumpRx cash prices for the same products run around $350. Medicare beneficiary copay caps at $50. Those numbers are not random. The $245 figure is roughly aligned with what other developed-market public payers pay for GLP-1s under their own price negotiation regimes. The $350 figure is a discount off list but still leaves meaningful margin in the cash channel. The $50 copay is the politically visible number that drives the press coverage and the patient-facing experience.

The implication for PBM economics is the part that does not get enough airtime in the consumer-facing coverage. If the public payer net price for GLP-1s is $245, the rebate spread that PBMs have been earning on those products gets compressed in a way that has knock-on effects across formulary positioning, exclusivity arrangements, and net cost calculations on the commercial side. Employer fiduciary obligations under ERISA become a much more uncomfortable place to sit when the public benchmark price is suddenly visible and lower than what the plan is paying. That sets up a litigation risk that is independent of the MFN program itself but accelerated by it.

The other thing worth flagging is the inclusion of future oral GLP-1s in the deal. That is not a small detail. The oral GLP-1 pipeline is where the next phase of the obesity and diabetes market gets fought, and locking in MFN pricing at launch for those products eliminates the standard playbook of high launch pricing followed by gradual rebate-driven net price compression. It changes the whole launch economics calculus for any oral GLP-1 entrant going forward, including the smaller biotechs that were planning to ride the slipstream of the Lilly and Novo branded launches.

The December nine and the J and J pickup

The December 2025 fact sheet was the largest single batch announcement of the program, covering nine companies in one tranche. Those nine were Amgen, Bristol Myers Squibb, Boehringer Ingelheim, Genentech, Gilead, GSK, Merck, Novartis, and Sanofi. The deal structure was the running Pfizer template: Medicaid MFN access on the existing portfolio, MFN at launch on new innovative medicines, and DTC discount routing through TrumpRx. The administration framed this as the largest set of developments to date in bringing MFN pricing to American patients, which was accurate in terms of company count but somewhat misleading in terms of underlying drug coverage, because the per-deal coverage varies and the public-facing fact sheets do not break it out at the SKU level.

Johnson and Johnson came in shortly after the December tranche, bringing the total to fifteen of the seventeen, as covered in AJMC’s reporting on the J and J agreement. That left AbbVie and Regeneron as the two final holdouts, which is a meaningful fact in itself. AbbVie’s exposure across Humira biosimilar dynamics, Skyrizi, Rinvoq, and the broader immunology portfolio made any MFN structure non-trivial to negotiate, and Regeneron’s positioning around Eylea and Praluent created its own set of pricing pressure points. The fact that those two companies held out longer than the others was a signal about deal complexity, not about whether they were going to come in at all.

Throughout this period the public-facing data on what each deal actually covered remained thin. The fact sheets named specific products in some cases, the TrumpRx browse page added drugs as deals were signed, and third-party reporting filled in the gaps inconsistently. There was no centralized place to see, for example, that BMS had committed to MFN pricing on a specific subset of its oncology portfolio with a specific rebate methodology against a specific reference country basket. Those details either did not exist in published form or were embedded in the bilateral contracts that the administration has not released.

TrumpRx and what is actually live on the page

TrumpRx is the consumer-facing piece of the program and the only place where the abstract pricing commitments turn into actual numbers a patient or an analyst can see and copy down. The browse page lists eighty drugs as of the most recent check, which is a useful artifact because it is the closest thing to a live view of what the manufacturers have actually agreed to put into the DTC channel. The drugs listed include Combigan, Toujeo, Mayzent, Cetrotide, Xigduo XR, Farxiga, Zeposia, Sotyktu, Humira, Wegovy, Ozempic, and a long tail of others spanning ophthalmology, endocrinology, neurology, immunology, fertility, and metabolic disease.

The platform itself is primitive. The browse experience is a flat list with cash prices and not much else. There is no integration with patient assistance programs, no real coordination with state Medicaid systems, no plan-level routing, and no clear handoff into the broader pharmacy benefit infrastructure. That primitiveness is both a feature and a liability. As a feature, it means TrumpRx can be stood up quickly and updated as deals close, which is what the administration needed politically. As a liability, it means the platform does not scale to the actual workflow that patients, prescribers, pharmacies, and payers need to make these prices usable in real life.

The bigger point is that TrumpRx as currently built is a placeholder. Somebody is going to build the real version. The real version needs eligibility verification, prescriber workflow integration, mail-order and specialty pharmacy fulfillment, real-time benefit comparison against existing plan coverage, secondary payer coordination for the Medicare and Medicaid populations, and audit-grade pricing transparency that can be used in fiduciary disputes. None of that exists today on TrumpRx, and none of it is in any of the public deal documents. That gap is where a meaningful chunk of the entrepreneurial opportunity sits, regardless of who ends up building it.

Regeneron and the closing of the cohort

The Regeneron deal closed the cohort on April 23, 2026, and the corresponding White House fact sheet from April 2026 is the document behind the screenshot that started a lot of the social media discussion. That fact sheet explicitly frames Regeneron as the seventeenth MFN deal and states that the seventeen leading pharmaceutical manufacturers represent eighty-six percent of the branded drug market. The named products and pricing details in the Regeneron deal are useful as a closing data point. Praluent, the PCSK9 inhibitor, gets cut from $537 to $225 through TrumpRx. All of Regeneron’s new medicines going forward get MFN pricing at launch. And Otarmeni, which is a smaller-volume product with a specific patient population, is provided free to US patients.

Reuters and STAT both reported on the Regeneron deal in April, with the STAT piece going into the most detail on the negotiation dynamics. The reporting confirms that Regeneron held out longer than most of the cohort because of the specific pricing pressure points around Eylea and the broader retinal disease portfolio. The deal as signed appears to have addressed the Praluent and Otarmeni pieces directly while leaving more granular Eylea-specific pricing to bilateral negotiation that has not been disclosed publicly.

What the Regeneron fact sheet does, beyond closing the cohort, is provide the eighty-six percent market coverage number. That is the cleanest single metric the administration has put out for the whole program. It is also a number worth being a little careful with, because branded drug market share is not the same as total prescription volume share, and it does not capture the specialty versus retail mix or the public versus commercial payer mix. Eighty-six percent of the branded market is meaningful. It is not the same as eighty-six percent of US prescription drug spending, which depending on how you cut it is somewhere in the high seventies once you account for biosimilar penetration, generic dominance in the retail channel, and the segments of the branded market not covered by the seventeen.

What is in the deals and what is conspicuously missing

The deals are bilateral and confidential, which means the public-facing artifacts are the fact sheets and the TrumpRx browse page rather than any contract text. Drug-level coverage varies meaningfully across manufacturers. Some deals appear to cover the bulk of a manufacturer’s portfolio with MFN pricing on Medicaid and DTC discounts. Others appear to cover a narrower subset of selective SKUs with specific carve-outs. The fact sheets do not break this out at the level of detail anybody trying to model net pricing impact actually needs.

The framing that the administration has used, which is some version of the lowest prices in American history, applies primarily to Medicaid pricing and to select DTC offerings. It does not apply to commercial plan pricing in any direct way, and it does not apply to the bulk of US prescription spending because generics already dominate over ninety percent of total prescription volume. The MFN program touches the branded portion of the market, and within that portion it touches specific channels (Medicaid and DTC) more directly than others (commercial PBM-intermediated). That is not a criticism of the program. It is just a more accurate framing of what the deals actually do, which matters when modeling impact rather than scoring political points.

The AMCP analysis flagged the most important gaps directly. There is no published full contract text. There is no published reference country basket, meaning nobody outside the negotiation knows which countries’ prices are being used as the MFN benchmark. There is no published MFN calculation formula, which matters a lot because the difference between using a strict minimum versus a weighted average versus a basket median produces meaningfully different price points. There is no published state Medicaid implementation guidance, meaning the actual rebate reconciliation mechanics across fifty different state Medicaid programs are still being worked out. And there is no published drug-by-drug schedule, meaning anyone trying to calculate manufacturer-level revenue impact has to make assumptions about coverage scope that may or may not match what is actually in the contracts.

That set of gaps is where the analytical work has to focus, and it is also where the infrastructure opportunity sits. Somebody has to build the tooling that fills those gaps, because the manufacturers, the states, the PBMs, the employers, and the eventual Medicare touchpoints all need that information to operate.

IRA plus MFN as a quasi-voluntary hybrid

The structural way to think about this program is as a hybrid that sits on top of the Inflation Reduction Act’s Medicare drug price negotiation framework. The IRA gave HHS statutory authority to negotiate prices on a defined set of high-spend Medicare Part D drugs, with the price applicable across Medicare and tied to a defined methodology. The MFN program sits next to that as an executive-leverage tool that uses tariff threats, manufacturing onshoring, and the implicit rulemaking lever to extract pricing concessions across a broader set of channels and products.

The combination is unusual. The IRA is statutory and slow. It applies to a narrow product list per year, with the negotiation cycle stretching across multiple years and the maximum fair price taking effect after extended notice periods. The MFN program is executive and fast. It applies to whichever manufacturers come to the table, on whichever channels they agree to, with pricing taking effect on whatever timeline gets negotiated bilaterally. The two together cover more ground than either could on its own, and they create different exposure profiles for different manufacturers depending on portfolio mix.

The quasi-voluntary nature is worth dwelling on. None of the seventeen agreements are technically required by statute. They are extracted through the credible threat of regulatory action and trade pressure that would be more painful and less negotiable than the deal on offer. That is a different compliance dynamic than what the IRA produces. It also creates a different durability profile. A future administration could in theory unwind the MFN agreements faster than they could unwind the IRA framework, because the MFN structure does not have the same statutory anchor. That political risk is one of the things any analysis of the long-term durability of this pricing regime has to factor in.

The trade-policy bundling matters here too. The deals come paired with tariff exemptions on pharmaceutical inputs and manufacturing investment commitments in the US. That bundling makes the deals more durable in practice than they would be on pricing alone, because unwinding the pricing piece without unwinding the trade and manufacturing piece would create a coordination problem the manufacturers could exploit. It also means the program has a constituency outside HHS, which is unusual for a drug pricing reform and which probably extends its political half-life by several years.

The new adjudication layer and where the infrastructure gets built

The interesting business question is not whether drug prices went down. It is what new infrastructure gets built to operationalize MFN across the channels and over time. The answer is that the program creates a new adjudication layer that sits between manufacturer price commitments, Medicaid net pricing, DTC cash channels, international reference prices, and eventually Medicare and ERISA purchasing behavior. That adjudication layer needs real software to function, and most of it does not exist today.

The first piece is MFN price benchmarking. Real-time international price normalization is hard. Different countries publish different price points (list, net, ex-manufacturer, public payer), in different currencies, with different rebate structures, on different release schedules. Building a benchmarking engine that produces a defensible MFN reference price for a specific drug at a specific point in time is non-trivial software work and has to handle purchasing power parity adjustments, rebate normalization, and net price estimation where public data is incomplete. That is a real product category and it does not exist at production scale today.

The second piece is contract arbitration and compliance tooling. The agreements are bilateral, but the compliance burden is multilateral. Manufacturers have to honor MFN commitments across Medicaid (fifty states, each with its own rebate reconciliation), DTC (TrumpRx and successor platforms), and any other channels included in the deal. State Medicaid agencies have to verify that the rebates they are receiving actually reflect the MFN commitment. The administration has to be able to audit compliance. Nobody has built a piece of software that does all of this end-to-end, and the absence of published contract text makes the build harder, not easier.

The third piece is Medicaid and DTC routing. TrumpRx is the placeholder version. The real version needs eligibility verification, prescriber workflow integration, secondary payer coordination, and audit-grade pricing transparency. It also needs to coexist with the existing pharmacy benefit infrastructure rather than try to replace it, because the workflow lock-in that PBMs have built over decades is not going to break overnight just because there is a cheaper cash price available somewhere else. The platform that figures out how to slot into existing workflows while still capturing the MFN price advantage is the one that wins.

The fourth piece is employer fiduciary tooling, which is probably the biggest of the infrastructure layers in dollar terms. ERISA imposes fiduciary obligations on employer health plans, and the recent wave of pharmacy benefit fiduciary litigation (the Wells Fargo case being the most visible example) has put plan sponsors on notice that paying above-market prices for prescription drugs is a real liability exposure. When MFN creates a publicly visible benchmark price for a meaningful subset of branded drugs, the difference between what the plan is paying and what the MFN benchmark says is reasonable becomes a litigation-grade data point. The tooling that surfaces that gap, helps plan sponsors document their decision-making, and routes patients to lower-cost channels where appropriate is the kind of thing that has both legal urgency and clear willingness-to-pay attached to it.

The fifth piece is drug-level arbitrage and channel optimization. As the MFN structure matures, opportunities will emerge to route specific patients to specific channels based on drug, plan, eligibility, and price point. Cross-border price indexing engines, real-time benefit routing tools, and specialty carve-out optimization platforms will all become necessary as the channel landscape gets more complex. The patient experience layer for navigating which drug should be filled where is going to be a real product category, and the entrant that builds it with audit-grade methodology rather than marketing veneer is going to be the one that captures the institutional buyers.

Open questions, gaps, and what to watch next

A few things are worth watching closely as the program moves from announcement to operation. The first is the underlying contract text. As of now, none of the bilateral agreements have been published in full, and the AMCP analysis correctly flags that until the contracts are public, any analysis of actual pricing impact has to rely on the fact sheets and reporting. If and when contract text becomes public, the pricing methodology and reference country basket will be the key things to look at, because those determine whether the MFN benchmark is a real economic floor or just a rhetorical anchor.

The second is state Medicaid implementation. The deals commit manufacturers to MFN pricing on Medicaid, but the actual rebate mechanics flow through state Medicaid programs with their own supplemental rebate negotiations, formulary structures, and reconciliation processes. The states are going to have to operationalize this, and the variation in how different states handle it will create real differences in actual realized pricing. Watching how the largest Medicaid markets (California, New York, Texas, Florida) implement the MFN commitments will be informative, because what they do is going to set the template for the smaller states.

The third is TrumpRx evolution. The platform as it exists today is too primitive to handle real-volume DTC fulfillment. Either the administration builds it out or somebody else does. The question is whether the eventual real version is a government platform, a private platform with government endorsement, or a fragmented set of manufacturer-direct platforms that all interoperate with TrumpRx as a price discovery layer. Each of those outcomes has different implications for who captures value in the channel and where the workflow integration burden lands.

The fourth is commercial spillover. The deals as signed do not directly require MFN pricing in commercial plans, but the public visibility of MFN reference prices changes the negotiating dynamic for commercial PBM contracts. Plan sponsors are going to start asking why they are paying more than the public benchmark. That conversation is going to drive a lot of the actual net price compression in the commercial channel, even though it is not in any of the deal documents and will not show up in any White House fact sheet.

The fifth is pipeline implications. The deals lock in MFN pricing at launch for new innovative medicines, which changes the launch economics calculus for any new product coming out of the seventeen. That has effects on which therapeutic areas the manufacturers prioritize, how they think about US versus ex-US launch sequencing, and how they structure their pricing strategy for products in late-stage development. This is the part of the program with the longest tail and probably the largest cumulative impact, even though it is invisible in any single fact sheet and will not be measurable for several years.

The sixth, and the most important for anyone trying to make a real return on this regulatory shift, is the infrastructure stack. The benchmarking engines, the compliance tooling, the routing platforms, the fiduciary analytics, and the channel optimization tools all need to get built. The companies that build them well, with primary-source data and audit-grade methodology, are going to have a meaningful run. That is the actual investment angle, and it is what most of the social media coverage of the program completely misses while arguing about whether the price cuts are real or theatrical. Both can be true at once, and the entrepreneurs who recognize that are the ones who will end up with something to show for it five years from now.

So is this bad for commercial payers and PBMs?